Money laundering is the process of concealing the origins of money obtained illegally by passing it through a complex sequence of banking transfers or commercial transactions. One problem of criminal activities is accounting for the proceeds without raising the suspicion of law enforcement agencies

Introduction

The comparison of regulatory regimes for Money Laundering and Corporate Crimes is an interesting one given that, first of all, the former is a crime committed by a natural person and the latter encompasses an umbrella of crimes committable by the corporate entity. This means that analysis of each will result in the observation of potential flaws in the current regulatory regimes and that these will differ profoundly. It therefore begs the question as to whether the seriousness of the latter can be assessed in summary form and if this is achievable, whether the illusion of the existing perpetrating party is in itself a hindrance to any satisfactory serious dealing. Further to this, the difference between perpetrators means that the question of ‘the threat of punishment’ may not be easily reorganised into a sliding scale of severe to non-severe threats of punishment.

This paper will first of all define both crimes of Money Laundering and Corporate Crime and with specific examples the regulatory regimes for both will be stated via analysis of specific examples. In order to determine whether offenders are dealt with in an equally serious manner, attention will be paid to the possible forms of punishment and how these differ in relation to natural and corporate entities. Finally, this question of possible forms will be a key issue in the analysis of whether or not the threat of punishment in relation to some crimes outweighs the others.

A. Regulatory Regimes in Place for Money Laundering

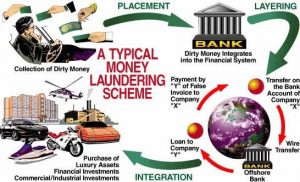

1. Definition of money laundering

Due to the apparent victimless nature of the crime of money laundering, it is often difficult to be able to grasp this concept fully. Article 1 of the draft European Communities (EC) Directive of March 1990 defines Money Laundering as:

“the conversion or transfer of property, knowing that such property is derived from serious crime, for the purpose of concealing or disguising the illicit origin of the property or of assisting any person who is involved in committing such an offence or offences to evade the legal consequences of his action,”

and

“the concealment or disguise of the true nature, source, location, disposition, movement, rights with respect to, or ownership of property, knowing that such property is derived from serious crime.”

This means that money laundering, as the term suggests, is the process of removing attention drawn to the handling of large sums of illegally obtained funds in order to prevent asset seizing. Money laundering is therefore an integral operation to the accumulation of profits in some of the world’s worst criminal activities such as organised crime, drug trafficking, terrorism and tax evasion.

2. The legislative framework for Money Laundering Offences

(a) The Proceeds of Crime Act 2002 Offences

This updated and expanded all of the various legislative measures and created a single source of legislation for general money laundering activities that are no longer related to a specific crime as was the case under the old regime which encompassed provisions under, among others, the Drug Trafficking Act 1994, the Criminal Justice Act 1988 (As amended by the Criminal Justice Act 1993) and the Prevention of Terrorism (Temporary Provisions) Act 1989.

Chapter seven of the Proceeds of Crime Act 2002 stipulates the three general money laundering offences which are concealment of criminal property , entering into or becoming concerned with a Money Laundering arrangement , and acquisition, use and possession of criminal property .

(i) Concealing

s 327of the 2002 Act stipulates that a person commits an offence if they:

“…conceal, disguise, convert or transfer criminal property or remove criminal property from England and Wales or from Scotland or from Northern Ireland…

(ii) Arrangements

Under this offence, it is a requirement for the prosecutor to establish that a person:

“…entered into or became concerned in an arrangement which they knew or suspected would facilitate another to acquire, retain, use or control criminal property… ”

It is also a requirement that the individual concerned also knew or suspected that the property was the benefit yielded from criminal conduct.

(iii) Acquisition, Use and Possession of Criminal Property

Where a person knows or suspects that property acquired constitutes a benefit of crime, they commit an offence under s 329 of the 2002 Act.

The same defences against committing the offence apply as in ss327 and 328, including those regarding authorised disclosure and appropriate consent. There is also a defence of ‘adequate consideration’ in s329(2)(c) so that persons who are paid for ordinary consumable goods and services in money that comes from crime are not under any obligation to question the source of the money. However, s329(3)(c) makes it clear that the provision by a person of goods or services which they know or suspect may help another to carry out criminal conduct is not consideration. Section 329(3) also sets out what the court will consider to be inadequate consideration such that the defence would not apply.

(b) Offences relating to failure of disclosure and tipping

Interestingly, failure to disclose has been expanded to cover three separate headings of regulated regimes , nominated officers in the regulated sector and other nominated officers . Of particular importance is the new crime of failure to report suspicions of money laundering of any proceeds of crime as opposed suspicion in relation to the proceeds of terrorism or drugs offences, as was specified under the old legislation.

In relation to the tipping off of individuals involved in Money Laundering activities, an offence is constituted if he discloses to the extent that an investigation is jeopardised as a result of an authorised disclosure having taken place to the relevant authorities .

(c) Penalties

The penalties for the above offences are the most crucial element in the argument for the threat of punishment. The penalties remain unchanged from the previous law and are found under s 334 of the 2002 Act. Penalties for offences under ss327-329 of the 2002 Act are up to fourteen years on indictment to imprisonment or a fine or both. As for offences under ss330-333 there exists a penalty is liable on indictment of imprisonment for a maximum of five years or a fine or both.

(d) The Money Laundering Regulations 2003

The Money Laundering Regulations 2003 acts to expand applicable businesses in the regulated sector to include, all relevant businesses, which are defined under Regulation 2(2) and includes national savings banks, loans companies, the bureau d’change, estate agents and casinos, to name but a few. There is a strict regulatory requirement for any person conducting business where there is a transaction of cash that exceeds fifteen thousand euros .

The key indication of these provisions is the direct desire to explicitly expand the regulatory regimes to all businesses that would engage in large transactions and therefore oblige them to be aware of money laundering and the obligation to blow the whistle where necessary.

Conclusion to Part A

Here it is clear that the regulatory regimes of Money Laundering have a clear and broad reach with the double aim of making sure that there is no smooth acquisition of the proceeds of crime as well as no ignorance on the part of those that would otherwise turn a blind eye to such activity. Therefore, as a forefront thought to the comparative analysis of corporate crime, it is crucial to know that the current analysis of Money Laundering regimes reveals a clear scare tactic for fear of punishment for failure to disclose and tipping offences.

B. Comparison with Regulatory Regimes in Place for Corporate Crimes

1 What is corporate crime?

Corporate Crime, i.e. crime that is committed by the separate legal identity, is an interesting phenomenon for the reason that, not only does it fully endorse the Soloman v Soloman concept of the separate legal entity it takes this concept to another level and accepts that it is possible to convict this fictional character for a crime.

2 Current Problems with Corporate Crime

(a) Regulatory crimes versus mens rea offences

The conviction of a company for regulatory, strict liability offences that require no mens rea is non-problematic for two main reasons. The first is that there is no need to ascertain mens rea and the second is that the crime is usually not a serious one, with the result that issues of replacing imprisonment with an unfathomable fine that would suit company is equally unproblematic.

However with reference to specific examples regarding mens rea crimes, it becomes clear that corporate conviction are attempted where there is no singularly blameworthy natural person. This occurred in the case of Tesco v Natrass , which involved an industrial accident that resulted in the death of an employee. There is an extremely fine line between this and the situation where there is not enough evidence to track down the human perpetrator or perpetrators, so recourse is made to the corporation. An example that definitely sways in the direction of the former is that of Corporate Manslaughter where an industrial accident occurs as a result of administrative failure in the efficient carrying out of health and safety measures. The crime therefore is the result of engrained flaws in the administrative running of the company’s health and safety procedures. Another example is the case of Dean v John Menzies Holdings Ltd which was an attempt to find a corporation guilty of shameless indecency. The actual pinpointing of the individual who had admitted certain pornography for sale was not even an issue of the court.

Neither of these cases were successful on the grounds that there was no ascertainable method of attributing natural mens rea to corporations as the ‘directing mind and will’ of the company could not be ascertained due to a lack of documentary evidence. This therefore asks two specific questions.

(b) By comparison to Money Laundering offences, is Corporate Crime conceivable?

By comparison to the rather clean structure of the Money Laundering regulation regime there is no such specialization for corporate crimes. Currently, as seen by the above examples, there is merely the common law attempt to force these crimes like jigsaw pieces into incompatible gaps in the puzzle of corporate accountability for criminal activity.

In addition to a complete lack of specialised legislation the common law fails profoundly to find a solution to the question of mens rea with the result that, far from providing equal treatment to offenders, a corporation cannot be found guilty at all!

Separate legal identity is a fantastic mechanism for the facilitation of financial liability severance by the directors from the expenses and risks the company. The TRUE natural minds of the company are therefore less tentative to take calculated equity and debt financing risks and this is a huge benefit to the economy. To therefore suggest that, in addition to a separate credit rating, that the company is also capable of having a criminal record, is out of the question.

(b) Can the problems of sentencing be resolved?

Corporations cannot of course be imprisoned with the result that deprivation of money in the form of penalties is the only route to punishment. The neat sentencing provisions of Money Laundering are of a type for which there can be no corporate alternative other than an unquantifiable fine. The result is a lack of justice for those affected by the worst of corporate crimes, such as corporate manslaughter. (despite the fact that no conviction has yet been secured). Corporations are also extremely clever, with the result that any smart move to create new forms of punishment, such as the removal of a sound credit rating or compulsory liquidation would result in the operations of the black listed or liquidated company being run by a new entity or shifted to another subsidiary.

Conclusion

The result of the problems with corporate crime reveal that this type of crime is very much a work in progress and this makes comparison with money laundering very difficult. The difference is that both are capable of being crimes that form the poison of any corporate administration but the threat of personal punishment makes the crime of money laundering far more real. By comparison, it can be concluded that there is wholly unequal treatment of perpetrators since, while the money launderers are convicted, the corporations are acquitted. In conclusion, journalistic ridicule and the threat of forced resignation is currently the only available form of punishment that, despite its unofficial nature, would be a strong enough scare tactic for corporations.

Bibliography

Legislation

- Money Laundering Regulations 2003

- Proceeds of Crime Act 2002

- Drug Trafficking Act 1994

- Criminal Justice Act 1988 (As amended by the Criminal Justice Act 1994)

- Prevention of Terrorism (Temporary Provisions) Act 1989

Case Law

- Salomon v Salomon & Co Ltd [1897] AC 22

- Tesco v Nattrass [1972] AC 153

- Dean v John Menzies Holdings Ltd 1981 JC 23

Text Book Publications

- D Masciandaro, “Global Financial Crime, Terrorism, Money Laundering and Offshore Centres,” (Ashgate, 2004)

- G Slapper, “Corporate Crime,” (Longman, 1999)

Conference Papers

- Money Laundering – Best Practice and Latest Developments

Article

- Irwin Mitchell, “UK Corporate Compliance & Regulation articles in association with the Legal500. www.legal500.com