Corporate finance is the study of a business’s money-related decisions, which are essentially all of a business’s decisions. Despite its name, corporate finance applies to all businesses, not just corporations. The primary goal of corporate finance is to figure out how to maximize a company’s value by making good decisions about investment, financing and dividends. In other words, how should businesses allocate scarce resources to minimize expenses and maximize revenues? How should companies acquire these resources – through stock or bonds, owner capital or bank loans? Finally, what should a company do with its profits? How much should it reinvest into the company, and how much should it pay out to the business’s owners? This walkthrough will explore each of these business decisions in greater depth.

A business can be organized in one of several ways, and the form its owners choose will affect the company’s and owners’ legal liability and income tax treatment. Here are the most common options and their major defining characteristics.

Sole Proprietorship

The default option is to be a sole proprietor. With this option there are fewer forms to file than with other business organizations. The business is structured in such a manner that legal documents are not required to determine how profit-sharing from business operations will be allocated.

This structure is acceptable if you are the business’s sole owner and you do not need to distinguish the business from yourself. Being a sole proprietor does not preclude you from using a business name that is different from your own name, however. In a sole proprietorship all profits, losses, assets and liabilities are the direct and sole responsibility of the owner. Also, the sole proprietor will pay self-employment tax on his or her income.

Sole proprietorships are not ideal for high-risk businesses because they put your personal assets at risk. If you are taking on significant amounts of debt to start your business, if you’ve gotten into trouble with personal debt in the past or if your business involves an activity for which you might potentially be sued, then you should choose a legal structure that will better protect your personal assets. Nolo, a company whose educational books make legal information accessible to the average person, gives several examples of risky businesses, including businesses that involve child care, animal care, manufacturing or selling edible goods, repairing items of value, and providing alcohol. These are just a few examples. There are many other activities that can make your business high risk.

If the risks in your line of work are not very high, a good business insurance policy can provide protection and peace of mind while allowing you to remain a sole proprietor. One of the biggest advantages of a sole proprietorship is the ease with which business decisions can be made.

LLC

An LLC is a limited liability company. This business structure protects the owner’s personal assets from financial liability and provides some protection against personal liability. There are situations where an LLC owner can still be held personally responsible, such as if he intentionally does something fraudulent, reckless or illegal, or if she fails to adequately separate the activities of the LLC from her personal affairs.

This structure is established under state law, so the rules governing LLCs vary depending on where your business is located. According to the IRS, most states do not allow banks, insurance companies or nonprofit organizations to be LLCs.

Because an LLC is a state structure, there are no special federal tax forms for LLCs. An LLC must elect to be taxed as an individual, partnership or corporation. You will need to file paperwork with the state if you want to adopt this business structure, and you will need to pay fees that usually range from $100 to $800. In some states, there is an additional annual fee for being an LLC.

You will also need to name your LLC and file some simple documents, called articles of organization, with your state. Depending on your state’s laws and your business’s needs, you may also need to create an LLC operating agreement that spells out each owner’s percentage interest in the business, responsibilities and voting power, as well as how profits and losses will be shared and what happens if an owner wants to sell her interest in the business. You may also have to publish a notice in your local newspaper stating that you are forming an LLC.

Corporation

Like the LLC, the corporate structure distinguishes the business entity from its owner and can reduce liability. However, it is considered more complicated to run a corporation because of tax, accounting, record keeping and paperwork requirements. Unless you want to have shareholders or your potential clients will only do business with a corporation, it may not be logical to establish your business as a corporation from the start – an LLC may be a better choice.

The steps for establishing a corporation are very similar to the steps for establishing an LLC. You will need to choose a business name, appoint directors, file articles of incorporation, pay filing fees and follow any other specific state/national requirements. (Find out how becoming a corporation can protect and further your finances. See Should You Incorporate Your Business?)

There are two types of corporations: C corporations (C corps) and S corporations (S corps). C corporations are considered separate tax-paying entities. C corps file their own income tax returns, and income earned remains in the corporation until it is paid as a salary or wages to the corporation’s officers and employees. Corporate income is often taxed at lower rates than personal income, so you can save money on taxes by leaving money in the corporation.

If you’re only making enough to get by, however, this won’t help you because you’ll need to pay almost all of the corporation’s earnings to yourself. If the corporation has shareholders, corporate earnings become subject to double taxation in the sense that income earned by the corporation is taxed and dividends distributed to shareholders are also taxed. However, if you are a one-person corporation, you don’t have to worry about double taxation.

S corporations are pass-through entities, meaning that their income, losses, deductions and credits pass through the company and become the direct responsibility of the company’s shareholders. The shareholders report these items on their personal income tax returns, thus S corps avoid the income double taxation that is associated with C corps.

All shareholders must sign IRS form 2553 to make the business an S corp for tax purposes. The IRS also requires S corps to meet the following requirements:

- Be a domestic corporation

- Have only allowable shareholders, including individuals, certain trusts and estates

- Not include partnerships, corporations or non-resident alien shareholders

- Have no more than 100 shareholders

- Have one class of stock

- Not be an ineligible corporation (i.e., certain financial institutions, insurance companies and domestic international sales corporations)

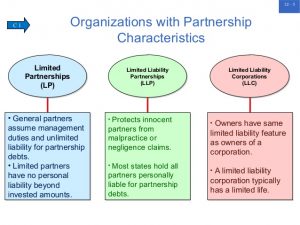

General Partnerships, Limited Partnerships (LP) and Limited Liability Partnerships (LLP)

A partnership is a structure appropriate to use if you are not going to be the sole owner of your new business.

In a general partnership, all partners are personally liable for business debts, any partner can be held totally responsible for the business and any partner can make decisions that affect the whole business.

In a limited partnership, one partner is responsible for decision-making and can be held personally liable for business debts. The other partner merely invests in the business. Although the general structure of limited partnerships can vary, each individual is liable only to the extent of their invested capital.

LLPs are most commonly used by professionals such as doctors and lawyers. The LLP structure protects each partner’s personal assets and each partner from debts or liability incurred by the other partners. Different states have varying regulations regarding these establishments of which business owners must take note.

Partnerships must file information returns with the IRS, but they do not file separate tax returns. For tax purposes, the partnership’s profits or losses pass through to its owners, so a partnership’s income is taxed at the individual level. LPs and LLPs are also state entities and must file paperwork and pay fees similar to those involved in establishing an LLC.

Regardless of the way a business is structured, its owners will have the same overarching goals when it comes to the company’s financial management.

All businesses aim to maximize their profits, minimize their expenses and maximize their market share. Here is a look at each of these goals.

Maximize Profits A company’s most important goal is to make money and keep it. Profit-margin ratios are one way to measure how much money a company squeezes from its total revenue or total sales.

There are three key profit-margin ratios: gross profit margin, operating profit margin and net profit margin.

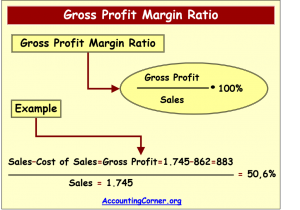

1. Gross Profit Margin

The gross profit margin tells us the profit a company makes on its cost of sales or cost of goods sold. In other words, it indicates how efficiently management uses labor and supplies in the production process.

| Gross Profit Margin = (Sales – Cost of Goods Sold)/Sales |

Suppose that a company has $1 million in sales and the cost of its labor and materials amounts to $600,000. Its gross margin rate would be 40% ($1 million – $600,000/$1 million).

The gross profit margin is used to analyze how efficiently a company is using its raw materials, labor and manufacturing-related fixed assets to generate profits. A higher margin percentage is a favorable profit indicator.

Gross profit margins can vary drastically from business to business and from industry to industry. For instance, the airline industry has a gross margin of about 5%, while the software industry has a gross margin of about 90%.

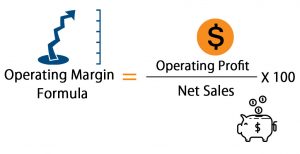

2. Operating Profit Margin

By comparing earnings before interest and taxes (EBIT) to sales, operating profit margins show how successful a company’s management has been at generating income from the operation of the business:

| Operating Profit Margin = EBIT/Sales |

If EBIT amounted to $200,000 and sales equaled $1 million, the operating profit margin would be 20%.

This ratio is a rough measure of the operating leverage a company can achieve in the conduct of the operational part of its business. It indicates how much EBIT is generated per dollar of sales. High operating profits can mean the company has effective control of costs, or that sales are increasing faster than operating costs. Positive and negative trends in this ratio are, for the most part, directly attributable to management decisions.

Because the operating profit margin accounts for not only costs of materials and labor, but also administration and selling costs, it should be a much smaller figure than the gross margin.

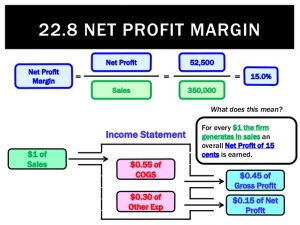

3. Net Profit Margin

Net profit margins are those generated from all phases of a business, including taxes. In other words, this ratio compares net income with sales. It comes as close as possible to summing up in a single figure how effectively managers run the business:

| Net Profit Margins = Net Profits after Taxes/Sales |

If a company generates after-tax earnings of $100,000 on its $1 million of sales, then its net margin amounts to 10%.

Often referred to simply as a company’s profit margin, the so-called bottom line is the most often mentioned when discussing a company’s profitability.

Again, just like gross and operating profit margins, net margins vary between industries. By comparing a company’s gross and net margins, we can get a good sense of its non-production and non-direct costs like administration, finance and marketing costs.

For example, the international airline industry has a gross margin of just 5%. Its net margin is just a tad lower, at about 4%. On the other hand, discount airline companies have much higher gross and net margin numbers. These differences provide some insight into these industries’ distinct cost structures: compared to its bigger, international cousins, the discount airline industry spends proportionately more on things like finance, administration and marketing, and proportionately less on items such as fuel and flight crew salaries.

In the software business, gross margins are very high, while net profit margins are considerably lower. This shows that marketing and administration costs in this industry are very high, while cost of sales and operating costs are relatively low.

When a company has a high profit margin, it usually means that it also has one or more advantages over its competition. Companies with high net profit margins have a bigger cushion to protect themselves during the hard times. Companies with low profit margins can get wiped out in a downturn. And companies with profit margins reflecting a competitive advantage are able to improve their market share during the hard times, leaving them even better positioned when things improve again.

Like all ratios, margin ratios never offer perfect information. They are only as good as the timeliness and accuracy of the financial data that gets fed into them, and analyzing them also depends on a consideration of the company’s industry and its position in the business cycle. Margins tell us a lot about a company’s prospects, but not the whole story.

Minimize Costs

Companies use cost controls to manage and/or reduce their business expenses. By identifying and evaluating all of the business’s expenses, management can determine whether those costs are reasonable and affordable. Then, if necessary, they can look for ways to reduce costs through methods such as cutting back, moving to a less expensive plan or changing service providers. The cost-control process seeks to manage expenses ranging from phone, internet and utility bills to employee payroll and outside professional services.

To be profitable, companies must not only earn revenues, but also control costs. If costs are too high, profit margins will be too low, making it difficult for a company to succeed against its competitors. In the case of a public company, if costs are too high, the company may find that its share price is depressed and that it is difficult to attract investors.

When examining whether costs are reasonable or unreasonable, it’s important to consider industry standards. Many firms examine their costs during the drafting of their annual budgets.

Maximize Market Share

Market share is calculated by taking a company’s sales over a given period and dividing it by the total sales of its industry over the same period. This metric provides a general idea of a company’s size relative to its market and its competitors. Companies are always looking to expand their share of the market, in addition to trying to grow the size of the total market by appealing to larger demographics, lowering prices or through advertising. Market share increases can allow a company to achieve greater scale in its operations and improve profitability.

The size of a market is always in flux, but the rate of change depends on whether the market is growing or mature. Market share increases and decreases can be a sign of the relative competitiveness of the company’s products or services. As the total market for a product or service grows, a company that is maintaining its market share is growing revenues at the same rate as the total market. A company that is growing its market share will be growing its revenues faster than its competitors. Technology companies often operate in a growth market, while consumer goods companies generally operate in a mature market.

New companies that are starting from scratch can experience fast gains in market share. Once a company achieves a large market share, however, it will have a more difficult time growing its sales because there aren’t as many potential customers available.

Next we’ll take a look at the potential conflicts of interest that can arise in the management of a business’s finances.

An agency relationship occurs when a principal hires an agent to perform some duty. A conflict, known as an “agency problem,“ arises when there is a conflict of interest between the needs of the principal and the needs of the agent.

In finance, there are two primary agency relationships:

- Managers and stockholders

- Managers and creditors

1. Stockholders versus Managers

- If the manager owns less than 100% of the firm’s common stock, a potential agency problem between mangers and stockholders exists.

- Managers may make decisions that conflict with the best interests of the shareholders. For example, managers may grow their firms to escape a takeover attempt to increase their own job security. However, a takeover may be in the shareholders’ best interest.

2. Stockholders versus Creditors

- Creditors decide to loan money to a corporation based on the riskiness of the company, its capital structure and its potential capital structure. All of these factors will affect the company’s potential cash flow, which is a creditors’ main concern.

- Stockholders, however, have control of such decisions through the managers.

- Since stockholders will make decisions based on their best interests, a potential agency problem exists between the stockholders and creditors. For example, managers could borrow money to repurchase shares to lower the corporation’s share base and increase shareholder return. Stockholders will benefit; however, creditors will be concerned given the increase in debt that would affect future cash flows.

Motivating Managers to Act in Shareholders’ Best Interests

There are four primary mechanisms for motivating managers to act in stockholders’ best interests:

- Managerial compensation

- Direct intervention by stockholders

- Threat of firing

- Threat of takeovers

1. Managerial Compensation

Managerial compensation should be constructed not only to retain competent managers, but to align managers’ interests with those of stockholders as much as possible.

- This is typically done with an annual salary plus performance bonuses and company shares.

- Company shares are typically distributed to managers either as:

- Performance shares, where managers will receive a certain number shares based on the company’s performance

- Executive stock options, which allow the manager to purchase shares at a future date and price. With the use of stock options, managers are aligned closer to the interest of the stockholders as they themselves will be stockholders.

2. Direct Intervention by Stockholders

Today, the majority of a company’s stock is owned by large institutional investors, such as mutual funds and pensions. As such, these large institutional stockholders can exert influence on mangers and, as a result, the firm’s operations.

3. Threat of Firing

If stockholders are unhappy with current management, they can encourage the existing board of directors to change the existing management, or stockholders may re-elect a new board of directors that will accomplish the task.

4. Threat of Takeovers

If a stock price deteriorates because of management’s inability to run the company effectively, competitors or stockholders may take a controlling interest in the company and bring in their own managers.

In the next section, we’ll examine the financial institutions and financial markets that help companies finance their operations.

A financial institution is an establishment that conducts financial transactions such as investments, loans and deposits. Almost everyone deals with financial institutions on a regular basis. Everything from depositing money to taking out loans and exchanging currencies must be done through financial institutions. Here is an overview of some of the major categories of financial institutions and their roles in the financial system.

Commercial Banks

Commercial banks accept deposits and provide security and convenience to their customers. Part of the original purpose of banks was to offer customers safe keeping for their money. By keeping physical cash at home or in a wallet, there are risks of loss due to theft and accidents, not to mention the loss of possible income from interest. With banks, consumers no longer need to keep large amounts of currency on hand; transactions can be handled with checks, debit cards or credit cards, instead.

Commercial banks also make loans that individuals and businesses use to buy goods or expand business operations, which in turn leads to more deposited funds that make their way to banks. If banks can lend money at a higher interest rate than they have to pay for funds and operating costs, they make money.

Banks also serve often under-appreciated roles as payment agents within a country and between nations. Not only do banks issue debit cards that allow account holders to pay for goods with the swipe of a card, they can also arrange wire transfers with other institutions. Banks essentially underwrite financial transactions by lending their reputation and credibility to the transaction; a check is basically just a promissory note between two people, but without a bank’s name and information on that note, no merchant would accept it. As payment agents, banks make commercial transactions much more convenient; it is not necessary to carry around large amounts of physical currency when merchants will accept the checks, debit cards or credit cards that banks provide.

Investment Banks

The stock market crash of 1929 and ensuing Great Depression caused the United States government to increase financial market regulation. The Glass-Steagall Act of 1933 resulted in the separation of investment banking from commercial banking.

While investment banks may be called “banks,” their operations are far different than deposit-gathering commercial banks. An investment bank is a financial intermediary that performs a variety of services for businesses and some governments. These services include underwriting debt and equity offerings, acting as an intermediary between an issuer of securities and the investing public, making markets, facilitating mergers and other corporate reorganizations, and acting as a broker for institutional clients. They may also provide research and financial advisory services to companies. As a general rule, investment banks focus on initial public offerings (IPOs) and large public and private share offerings. Traditionally, investment banks do not deal with the general public. However, some of the big names in investment banking, such as JP Morgan Chase, Bank of America and Citigroup, also operate commercial banks. Other past and present investment banks you may have heard of include Morgan Stanley, Goldman Sachs, Lehman Brothers and First Boston.

Generally speaking, investment banks are subject to less regulation than commercial banks. While investment banks operate under the supervision of regulatory bodies, like the Securities and Exchange Commission, FINRA, and the U.S. Treasury, there are typically fewer restrictions when it comes to maintaining capital ratios or introducing new products.

Insurance Companies

Insurance companies pool risk by collecting premiums from a large group of people who want to protect themselves and/or their loved ones against a particular loss, such as a fire, car accident, illness, lawsuit, disability or death. Insurance helps individuals and companies manage risk and preserve wealth. By insuring a large number of people, insurance companies can operate profitably and at the same time pay for claims that may arise. Insurance companies use statistical analysis to project what their actual losses will be within a given class. They know that not all insured individuals will suffer losses at the same time or at all.

Brokerages

A brokerage acts as an intermediary between buyers and sellers to facilitate securities transactions. Brokerage companies are compensated via commission after the transaction has been successfully completed. For example, when a trade order for a stock is carried out, an individual often pays a transaction fee for the brokerage company’s efforts to execute the trade.

A brokerage can be either full service or discount. A full service brokerage provides investment advice, portfolio management and trade execution. In exchange for this high level of service, customers pay significant commissions on each trade. Discount brokers allow investors to perform their own investment research and make their own decisions. The brokerage still executes the investor’s trades, but since it doesn’t provide the other services of a full-service brokerage, its trade commissions are much smaller.

Investment Companies

An investment company is a corporation or a trust through which individuals invest in diversified, professionally managed portfolios of securities by pooling their funds with those of other investors. Rather than purchasing combinations of individual stocks and bonds for a portfolio, an investor can purchase securities indirectly through a package product like a mutual fund.

There are three fundamental types of investment companies: unit investment trusts (UITs), face amount certificate companies and managed investment companies. All three types have the following things in common:

- An undivided interest in the fund proportional to the number of shares held

- Diversification in a large number of securities

- Professional management

- Specific investment objectives

Let’s take a closer look at each type of investment company.

Unit Investment Trusts (UITs)

A unit investment trust, or UIT, is a company established under an indenture or similar agreement. It has the following characteristics:

- The management of the trust is supervised by a trustee.

- Unit investment trusts sell a fixed number of shares to unit holders, who receive a proportionate share of net income from the underlying trust.

- The UIT security is redeemable and represents an undivided interest in a specific portfolio of securities.

- The portfolio is merely supervised, not managed, as it remains fixed for the life of the trust. In other words, there is no day-to-day management of the portfolio.

Face Amount Certificates

A face amount certificate company issues debt certificates at a predetermined rate of interest. Additional characteristics include:

- Certificate holders may redeem their certificates for a fixed amount on a specified date, or for a specific surrender value, before maturity.

- Certificates can be purchased either in periodic installments or all at once with a lump-sum payment.

- Face amount certificate companies are almost nonexistent today.

Management Investment Companies

The most common type of investment company is the management investment company, which actively manages a portfolio of securities to achieve its investment objective. There are two types of management investment company: closed-end and open-end. The primary differences between the two come down to where investors buy and sell their shares – in the primary or secondary markets – and the type of securities the investment company sells.

- Closed-End Investment Companies: A closed-end investment company issues shares in a one-time public offering. It does not continually offer new shares, nor does it redeem its shares like an open-end investment company. Once shares are issued, an investor may purchase them on the open market and sell them in the same way. The market value of the closed-end fund’s shares will be based on supply and demand, much like other securities. Instead of selling at net asset value, the shares can sell at a premium or at a discount to the net asset value.

- Open-End Investment Companies: Open-end investment companies, also known as mutual funds, continuously issue new shares. These shares may only be purchased from the investment company and sold back to the investment company. Mutual funds are discussed in more detail in the Variable Contracts section.

Read more: Series 26 Exam Guide: Investment Companies

Nonbank Financial Institutions

The following institutions are not technically banks but provide some of the same services as banks.

Savings and Loans

Savings and loan associations, also known as S&Ls or thrifts, resemble banks in many respects. Most consumers don’t know the differences between commercial banks and S&Ls. By law, savings and loan companies must have 65% or more of their lending in residential mortgages, though other types of lending is allowed.

S&Ls emerged largely in response to the exclusivity of commercial banks. There was a time when banks would only accept deposits from people of relatively high wealth, with references, and would not lend to ordinary workers. Savings and loans typically offered lower borrowing rates than commercial banks and higher interest rates on deposits; the narrower profit margin was a byproduct of the fact that such S&Ls were privately or mutually owned.

Credit Unions

Credit unions are another alternative to regular commercial banks. Credit unions are almost always organized as not-for-profit cooperatives. Like banks and S&Ls, credit unions can be chartered at the federal or state level. Like S&Ls, credit unions typically offer higher rates on deposits and charge lower rates on loans in comparison to commercial banks.

In exchange for a little added freedom, there is one particular restriction on credit unions; membership is not open to the public, but rather restricted to a particular membership group. In the past, this has meant that employees of certain companies, members of certain churches, and so on, were the only ones allowed to join a credit union. In recent years, though, these restrictions have been eased considerably, very much over the objections of banks.

Shadow Banks

The housing bubble and subsequent credit crisis brought attention to what is commonly called “the shadow banking system.” This is a collection of investment banks, hedge funds, insurers and other non-bank financial institutions that replicate some of the activities of regulated banks, but do not operate in the same regulatory environment.

The shadow banking system funneled a great deal of money into the U.S. residential mortgage market during the bubble. Insurance companies would buy mortgage bonds from investment banks, which would then use the proceeds to buy more mortgages, so that they could issue more mortgage bonds. The banks would use the money obtained from selling mortgages to write still more mortgages.

Many estimates of the size of the shadow banking system suggest that it had grown to match the size of the traditional U.S. banking system by 2008.

Apart from the absence of regulation and reporting requirements, the nature of the operations within the shadow banking system created several problems. Specifically, many of these institutions “borrowed short” to “lend long.” In other words, they financed long-term commitments with short-term debt. This left these institutions very vulnerable to increases in short-term rates and when those rates rose, it forced many institutions to rush to liquidate investments and make margin calls. Moreover, as these institutions were not part of the formal banking system, they did not have access to the same emergency funding facilities. (Learn more in The Rise And Fall Of The Shadow Banking System.)

Next, let’s learn about the types of financial markets in which these financial institutions operate.

A financial market is a broad term describing any marketplace where buyers and sellers participate in the trade of assets such as equities, bonds, currencies and derivatives. Financial markets are typically defined by having transparent pricing, basic regulations on trading, costs and fees, and market forces determining the prices of securities that trade.

Financial markets can be found in nearly every nation in the world. Some are very small, with only a few participants, while others – like the New York Stock Exchange (NYSE) and the forex markets – trade trillions of dollars daily.

Investors have access to a large number of financial markets and exchanges representing a vast array of financial products. Some of these markets have always been open to private investors; others remained the exclusive domain of major international banks and financial professionals until the very end of the twentieth century.

Capital Markets

A capital market is one in which individuals and institutions trade financial securities. Organizations and institutions in the public and private sectors also often sell securities on the capital markets in order to raise funds. Thus, this type of market is composed of both the primary and secondary markets.

Any government or corporation requires capital (funds) to finance its operations and to engage in its own long-term investments. To do this, a company raises money through the sale of securities – stocks and bonds in the company’s name. These are bought and sold in the capital markets.

Stock Markets

Stock markets allow investors to buy and sell shares in publicly traded companies. They are one of the most vital areas of a market economy as they provide companies with access to capital and investors with a slice of ownership in the company and the potential of gains based on the company’s future performance.

This market can be split into two main sections: the primary market and the secondary market. The primary market is where new issues are first offered, with any subsequent trading going on in the secondary market.

Bond Markets

A bond is a debt investment in which an investor loans money to an entity (corporate or governmental), which borrows the funds for a defined period of time at a fixed interest rate. Bonds are used by companies, municipalities, states and U.S. and foreign governments to finance a variety of projects and activities. Bonds can be bought and sold by investors on credit markets around the world. This market is alternatively referred to as the debt, credit or fixed-income market. It is much larger in nominal terms that the world’s stock markets. The main categories of bonds are corporate bonds, municipal bonds, and U.S. Treasury bonds, notes and bills, which are collectively referred to as simply “Treasuries.” (For more, see the Bond Basics Tutorial.)

Money Market

The money market is a segment of the financial market in which financial instruments with high liquidity and very short maturities are traded. The money market is used by participants as a means for borrowing and lending in the short term, from several days to just under a year. Money market securities consist of negotiable certificates of deposit (CDs), banker’s acceptances, U.S. Treasury bills, commercial paper, municipal notes, eurodollars, federal funds and repurchase agreements (repos). Money market investments are also called cash investments because of their short maturities.

The money market is used by a wide array of participants, from a company raising money by selling commercial paper into the market to an investor purchasing CDs as a safe place to park money in the short term. The money market is typically seen as a safe place to put money due the highly liquid nature of the securities and short maturities. Because they are extremely conservative, money market securities offer significantly lower returns than most other securities. However, there are risks in the money market that any investor needs to be aware of, including the risk of default on securities such as commercial paper. (To learn more, read our Money Market Tutorial.)

Cash or Spot Market

Investing in the cash or “spot” market is highly sophisticated, with opportunities for both big losses and big gains. In the cash market, goods are sold for cash and are delivered immediately. By the same token, contracts bought and sold on the spot market are immediately effective. Prices are settled in cash “on the spot” at current market prices. This is notably different from other markets, in which trades are determined at forward prices.

The cash market is complex and delicate, and generally not suitable for inexperienced traders. The cash markets tend to be dominated by so-called institutional market players such as hedge funds, limited partnerships and corporate investors. The very nature of the products traded requires access to far-reaching, detailed information and a high level of macroeconomic analysis and trading skills.

Derivatives Markets

The derivative is named so for a reason: its value is derived from its underlying asset or assets. A derivative is a contract, but in this case the contract price is determined by the market price of the core asset. If that sounds complicated, it’s because it is. The derivatives market adds yet another layer of complexity and is therefore not ideal for inexperienced traders looking to speculate. However, it can be used quite effectively as part of a risk management program. (To get to know derivatives, read The Barnyard Basics Of Derivatives.)

Examples of common derivatives are forwards, futures, options, swaps and contracts-for-difference (CFDs). Not only are these instruments complex but so too are the strategies deployed by this market’s participants. There are also many derivatives, structured products and collateralized obligations available, mainly in the over-the-counter (non-exchange) market, that professional investors, institutions and hedge fund managers use to varying degrees but that play an insignificant role in private investing.

Forex and the Interbank Market

The interbank market is the financial system and trading of currencies among banks and financial institutions, excluding retail investors and smaller trading parties. While some interbank trading is performed by banks on behalf of large customers, most interbank trading takes place from the banks’ own accounts.

The forex market is where currencies are traded. The forex market is the largest, most liquid market in the world with an average traded value that exceeds $1.9 trillion per day and includes all of the currencies in the world. The forex is the largest market in the world in terms of the total cash value traded, and any person, firm or country may participate in this market.

There is no central marketplace for currency exchange; trade is conducted over the counter. The forex market is open 24 hours a day, five days a week and currencies are traded worldwide among the major financial centers of London, New York, Tokyo, Zürich, Frankfurt, Hong Kong, Singapore, Paris and Sydney.

Until recently, forex trading in the currency market had largely been the domain of large financial institutions, corporations, central banks, hedge funds and extremely wealthy individuals. The emergence of the internet has changed all of this, and now it is possible for average investors to buy and sell currencies easily with the click of a mouse through online brokerage accounts. (For further reading, see The Foreign Exchange Interbank Market.)

Primary Markets vs. Secondary Markets

A primary market issues new securities on an exchange. Companies, governments and other groups obtain financing through debt or equity based securities. Primary markets, also known as “new issue markets,” are facilitated by underwriting groups, which consist of investment banks that will set a beginning price range for a given security and then oversee its sale directly to investors.

The primary markets are where investors have their first chance to participate in a new security issuance. The issuing company or group receives cash proceeds from the sale, which is then used to fund operations or expand the business. (For more on the primary market, see our IPO Basics Tutorial.)

The secondary market is where investors purchase securities or assets from other investors, rather than from issuing companies themselves. The Securities and Exchange Commission (SEC) registers securities prior to their primary issuance, then they start trading in the secondary market on the New York Stock Exchange, Nasdaq or other venue where the securities have been accepted for listing and trading. (To learn more about the primary and secondary market, read Markets Demystified.)

The secondary market is where the bulk of exchange trading occurs each day. Primary markets can see increased volatility over secondary markets because it is difficult to accurately gauge investor demand for a new security until several days of trading have occurred. In the primary market, prices are often set beforehand, whereas in the secondary market only basic forces like supply and demand determine the price of the security.

Secondary markets exist for other securities as well, such as when funds, investment banks or entities such as Fannie Mae purchase mortgages from issuing lenders. In any secondary market trade, the cash proceeds go to an investor rather than to the underlying company/entity directly. (To learn more about primary and secondary markets, read A Look at Primary and Secondary Markets.)

The OTC Market

The over-the-counter (OTC) market is a type of secondary market also referred to as a dealer market. The term “over-the-counter” refers to stocks that are not trading on a stock exchange such as the Nasdaq, NYSE or American Stock Exchange (AMEX). This generally means that the stock trades either on the over-the-counter bulletin board (OTCBB) or the pink sheets. Neither of these networks is an exchange; in fact, they describe themselves as providers of pricing information for securities. OTCBB and pink sheet companies have far fewer regulations to comply with than those that trade shares on a stock exchange. Most securities that trade this way are penny stocks or are from very small companies.

Third and Fourth Markets

You might also hear the terms “third” and “fourth markets.” These don’t concern individual investors because they involve significant volumes of shares to be transacted per trade. These markets deal with transactions between broker-dealers and large institutions through over-the-counter electronic networks. The third market comprises OTC transactions between broker-dealers and large institutions. The fourth market is made up of transactions that take place between large institutions. The main reason these third and fourth market transactions occur is to avoid placing these orders through the main exchange, which could greatly affect the price of the security. Because access to the third and fourth markets is limited, their activities have little effect on the average investor.

Financial institutions and financial markets help firms raise money. They can do this by taking out a loan from a bank and repaying it with interest, issuing bonds to borrow money from investors that will be repaid at a fixed interest rate, or offering investors partial ownership in the company and a claim on its residual cash flows in the form of stock.