A charitable trust is an irrevocable trust established for charitable purposes and, in some jurisdictions, a more specific term than “charitable organization”. A charitable trust enjoys a varying degree of tax benefits in most countries. It also generates good will. Some important terminology in charitable trusts is the term ‘corpus’ (Latin for ‘body’) which refers to the assets with which the trust is funded and the term ‘donor’ which is the person donating assets to a charity.

Trust created for advancement of education, promotion of public health and comfort, relief of poverty, furtherance of religion, or any other purpose regarded as charitable in law. Benevolent and philanthropic purposes are not necessarily charitable unless they are solely and exclusively for the benefit of public or a class or section of it. Charitable trusts (unlike private or non-charitable trust) can have perpetual existence and are not subject to laws against perpetuity. They are wholly or partially exempt from almost all taxes. Where the purpose of a charitable trust becomes impossible or unpractical to carry out then, under the legal doctrine of cy près (French for, as near as), the trustees acting by a majority or a court may choose another charitable purpose as nearly like the original purpose as possible.

A Charitable trust is a trust for a purpose, but where the purpose is regarded as sufficiently beneficial to the community at large to warrant acceptance of validity. This means that if it perfectly possible to establish a trust for the achievement of a purpose, provided that the purpose in law is regarded as charitable. As far as charities are concerned, it is not important that there is o human beneficiary capable of enforcing the trust because the Attorney General may take action in respect of all charitable trusts subject to certain aspects of the perpetuity rule and may be of unlimited duration.

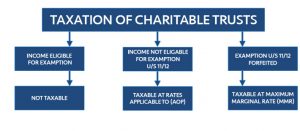

Taxation of Charitable Trusts

Charitable trusts are distinguishable from private trusts in many ways. First, charitable trusts may last in perpetuity because it is not contrary to public policy for the money to be permanently dedicated to a charitable purpose which is beneficial to the community and likewise a gift over from one charity to another, which could be triggered if the original charity should fail to observe some limitation placed on the use of the property by the donor, will not fail if it take effect outside the perpetuity period . This is because charity is regarded in law as indivisible, irrespective of the actual group or body carrying out the purpose. Secondly should a charitable trust fail the normal rules of resulting trusts may not apply. Thirdly, there are some differences in the way charitable trustees may administer a charitable trust and some difference in the scope of their powers ad duties.

The most important difference in relation to charitable trusts is that of relief from fiscal obligations and advantages that are received from charities.

1. New Dawn

Traditionally, charitable trusts are said to fall within four broad categories, being those that were identified by Lord Macaughten in Pemsel’s case : viz, trusts for the relief of poverty, trusts for the advancement of education; trusts for the advancement of religion; and finally trusts for other purposes beneficial to the community.

This fourfold classification represents a useful descriptive tool rather than a precise analysis of the meaning of charity . The most crucial point seems to be that for a trust to be charitable; it must fall within “the spirit and intendment” of the Preamble of 1601 and it is not enough simply that a purpose is beneficial to the community; it must be one which is beneficial and which the law regards as charitable. This is particularly important when considering the fourth category of charity referred to in Pemsel because not every purpose trust which confers a benefit to the community will be charitable , despite some suggestions to the contrary .

It may be that this trust is within the scope of trusts for the advancement of religion and is thereby charitable. There is no doubt here that the proposed trust is connected with a religious establishment and questions concerning the disputed status of some faiths and beliefs are not relevant . Yet, it is unclear whether trusts for religious purposes per se can be charitable if they are not otherwise for the advancement of religion

2. Democrac

There is first an argument here that this could fall within the category of education, however there is also an argument that this has political motivation. Each of these arguments will now be considered in turn.

The Preamble to the Statute of 1601 itself talks of “schools of learning”, and there is o doubt that the endowment of schools is a charitable purpose. There is however an argument that the charitable purpose is limited to a particular area and might fail the test of public benefit.

The class of persons who will receive such political education is fairly limited, and this may well be regarded as a class within a class and so too narrowly drawn to confer a benefit on the public, as in Williams Trustees v IRC . On the other hand, in this case, the door is not attempting to benefit persons with whom he is personally connected. In the end, it will be a matter of judgement, although if the donor wishes to avoid these problems he cold amend the class limiting factors.

It is possible that this might be regarded as a trust for the relief of poverty, in that it is for those in inner city schools. However, although the construction would avoid the “public benefit” difficulties just discussed, the better view is that the purpose of the trust is educational and that the disadvantaged nature of the persons who might benefit is a subsidiary factor. In sum, there is a good argument that this will be an educational charity, provided difficulties over the “public” nature of the benefits thereby conferred can be overcome.

3. Medi Aid

It is perfectly in order for a charitable trust to allow the trustees some discretion in the selection of charitable objects provided, of course, that the trustees are required by the trust to exercise that discretion in favour of objects that are exclusively charitable. In this particular cases there are two issues firstly whether the administration of treatment is in itself charitable and secondly, whether the trustees ability to use the money for those that have worked in the NHS has any bearing on whether or not this will or will not be a charitable trust.

As far as the administration of medication is concerned, this is likely to be a purpose that falls within the category of “other purposes beneficial to the community”, the fourth category that was identified in the case of Pemsel. This is despite the fact that there is some doubt as to how we are to determine whether any given purpose is charitable within this fourth class. According to Russell LJ in Incorporated Council for Law Reporting in England and Wales v Attorney General, a court is entitled to assume that if a purpose is in itself beneficial to the community that it is also charitable in law. On the other hand, the more traditional approach requires that there must be some precedent or analogy with the 1601 Preamble or previous case law before a new purpose which beneficial in itself can also be regarded as charitable .

When considering the fourth category of charity it is clear that the beneficial nature of the purpose needs to be positively established before its charitable status can be admitted. Traditionally, when determining whether any purpose was charitable within the fourth category, the courts would look to the Preamble of the Statute of Charitable Uses and previous cases, and then decide whether there was either a precedent or analogy for the charitable status of the new purpose . This could mean that a perfectly useful and worthy purpose might fail to be recognised as a charity simply because of a lack of existing precedent, although in practice this is highly unlikely given the wealth of material and the extensive discretion which judges enjoy. On this analysis it is likely that this proposed charity will be granted charitable status.

The second question which must now be considered is whether or not a sufficient section of the public benefit from this charitable purpose. The law admits the special status and privileges of charitable trusts only when the benefit is not confined to a few people with special status. This general statement of principle must be qualified for it is clear that charities for the relief of poverty are not subject to such a stringent test of public benefit as other types of charity .

To consider whether a charity is or is not for the public benefit there are some questions that must be answered. First, it is obvious that the benefits of a charitable trust must not be restricted to a group of people that are numerically negligible . The point is that the class of persons who may benefit from the charitable purpose must not be narrowly restricted by definition; it matters not that only a small group of people actually enjoy the benefits of the charitable purpose so long as those benefits are available to the public should they come forward . What is numerically negligible will depend on the facts of the case. Given here that the NHS is such a huge public organisation, it is extremely unlikely that the persons who can benefit will be numerically negligible.

The benefits derived from the charity may be limited to a class of persons . Although this can only be a “rule of thumb”, the idea is that one limitation on the class of persons who may derive a benefit from the charity does not destroy the “public” character of the trust, but that a second or third limitation may well make it so difficult for the public at large to qualify for the charitable benefitthat there is no real public benefit at all .

The third consideration that must be made is that a trust will not be regarded as charitable, if the potential class of persons likely to benefit are united by a common personal bond. This is known as the “Compton test ”, and it was confirmed by the House of Lords in Oppenheim. Essentially, the point is that if the class intended to benefit from the charity shares a common personal relationship- perhaps all employees of a company- they may not be capable of being regarded as a section of the public, even if numerically very great. However, there are difficulties here and there are doubts whether this “personal nexus” test is suitable to determine the public benefit. As must was stated in Dingle v Turner , although this case was concerned with the relief of poverty which is outside the test and therefore renders its criticisms of Oppenheim strictly obiter. One important criticism is that it is unclear exactly what the personal nexus test is designed to prevent.

On the basis of this personal nexus test it is likely that this charity will fail as it does not satisfy the requirements of public benefit as it is designed to benefit only those that have worked within the NHS.